Estimated reading time: 5 minutes

Listen to this podcast on Spotify, Apple Podcasts, Podbean, Podtail, ListenNotes, TuneIn

The volatility of the geopolitical and macroeconomic environment in recent years has caused some problems in the trade, treasury, and payments industries.

However, industry actors have adapted and are working together to build resilience and make international trade even stronger.

To hear about developments in the factoring and supply chain finance world, Trade Finance Global (TFG) spoke with Çağatay Baydar, Chairman at FCI and Irina Tyan, Principal Banker, TFP at the European Bank for Reconstruction and Development (EBRD).

Challenges and growth in the factoring industry

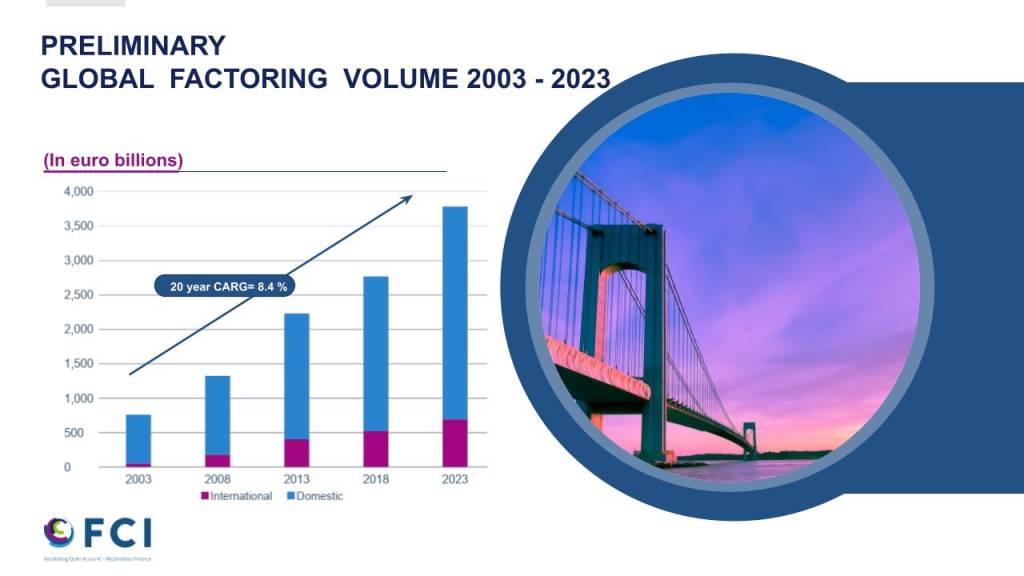

The factoring industry has demonstrated impressive growth since the turn of the century despite facing significant challenges, particularly in emerging markets.

Baydar said, “The growth rate in 2023 was 3.3% globally in the volume of the world factoring and in 2022 it was 18%. Over the last 20 years, the average growth rate has been 8% which shows that factoring is becoming a mainstream financial product globally, which is very good indeed.”

The sector, which revolves around the purchase of receivables from businesses to provide them with immediate liquidity, has become an essential component of global trade finance, but it also faces challenges. One of the primary challenges is the bureaucratic and infrastructural limitations inherent in the current system.

Factoring, being an invoice-based product, requires a significant amount of paperwork and documentation, which can be cumbersome and traditionally relies on a paper-based system that only adds to the administrative burden for businesses.

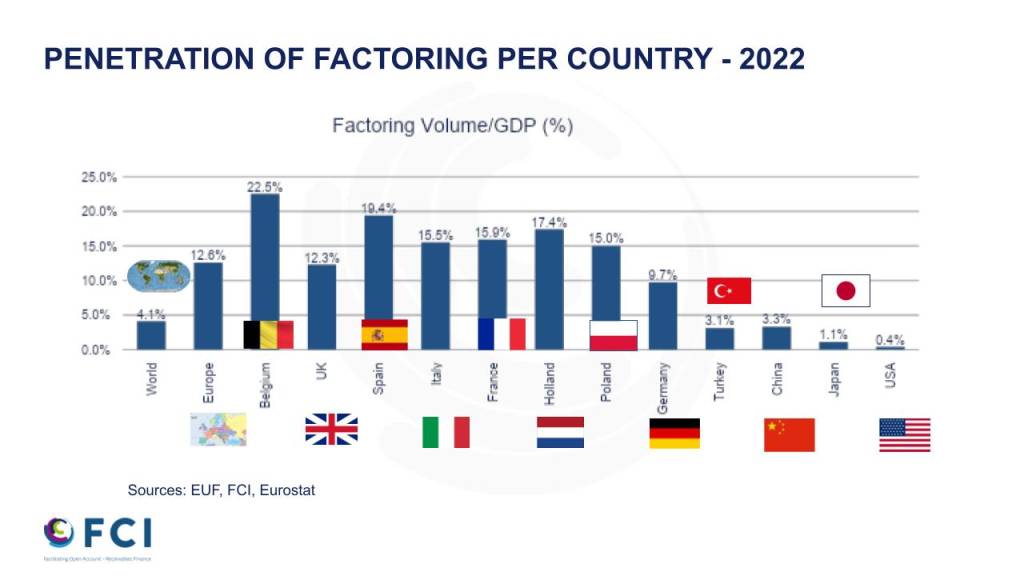

In developed regions like Europe, factoring’s penetration rate – a measure of the amount of trade volume that uses factoring – is around 15%, reflecting a more mature understanding and use of this financial product. By contrast, in emerging markets, the penetration rate is significantly lower, with countries like Turkey and Georgia showing rates as low as 3%.

This discrepancy highlights the knowledge gap and infrastructural deficiencies in these regions. Businesses in these markets often lack the necessary awareness and understanding of factoring, which limits their ability to leverage this financial tool to its full potential.

However, factoring usage in some emerging markets is growing.

Tyan said, “We see the progress in the countries where we started five to seven years ago, like Georgia. We recently had a workshop in Jordan, where we also see a more adapted market, more ready to look into this type of product.”

Further collaboration and efforts to promote regulatory reforms and technological advancements may be what is needed to drive factoring growth in these underutilised regions.

Regulatory reforms and technological integration

Regulatory reforms are crucial for the sustained growth and development of the factoring industry, and legal clarity is particularly important in emerging markets, where the absence of a well-defined regulatory environment can pose significant barriers to factoring’s growth.

One of the key areas that require attention is the standardisation of data exchange formats.

Creating common data standards for supply chain transactions can facilitate smoother integration between different platforms and financial institutions, improving efficiency, reducing administrative burdens, and enhancing the overall effectiveness of the factoring process.

Another important aspect of regulatory reform is cybersecurity.

Tyan said, “As this product heavily relies on platforms, clear regulation on data security and cybersecurity is crucial to build trust among the participants.”

Ensuring the integrity and security of transactions protects sensitive financial information from potential cyber threats and is vital for the long-term sustainability and credibility of the industry.

Digitalising to draw clients and talent to factor

The factoring industry has been significantly transformed by the integration of digital technologies that have made the process faster, more efficient, and more accessible, especially for small and medium-sized enterprises (SMEs).

Traditionally, the paperwork involved in factoring, particularly for international transactions, slowed down the process and added to its complexity but digital platforms are allowing for quicker access to funds and improving the overall client experience.

Baydar said, “Today, with digitalisation and the platforms, we are making our business much faster, quicker, and more effective. This really helps SMEs to touch the money very soon, very quickly. This makes our clients happier than before because they can experience a very fast, very effective, seamless transaction.”

This shift not only speeds up transactions but also minimises the risk of errors and fraud associated with manual paperwork and can help attract more young professionals to the industry.

Baydar said, “Young people prefer to work with new technology and high-level startup businesses rather than traditional models.”

The new generation of workers is drawn to innovation and technologically advanced sectors. By embracing digital advancements, the factoring industry can position itself as a forward-thinking and dynamic field, appealing to young talent looking for exciting career opportunities. This influx of new talent is essential for sustaining the industry’s growth and development in the long term.

Organisations that fail to embrace digitalisation risk being left behind in a rapidly evolving market, meaning that investing in digital solutions is not just an option but a necessity for the future of the factoring industry.