Australia

Australia Hong Kong

Hong Kong Japan

Japan Singapore

Singapore United Arab Emirates

United Arab Emirates United States

United States France

France Germany

Germany Ireland

Ireland Netherlands

Netherlands United Kingdom

United Kingdom

Invoice Finance

Welcome to TFG’s invoice finance hub. Find out how our team can help your company unlock working capital from domestic and international invoices, on both a recourse and non-recourse basis. Alternatively, learn more about the different types of invoice finance: discounting and factoring, through our latest research, information and insights, right here, in our invoice finance hub.

What is invoice finance?

Invoice finance is a common form of business finance where funds are advanced against unpaid invoices prior to customer payment. Invoice finance houses include banks, alternative investment providers and private lenders, used by businesses who trade both domestically and globally. There are two types of invoice financing methods; discounting and factoring. Invoice finance is a type of receivables finance (more info on receivables here).

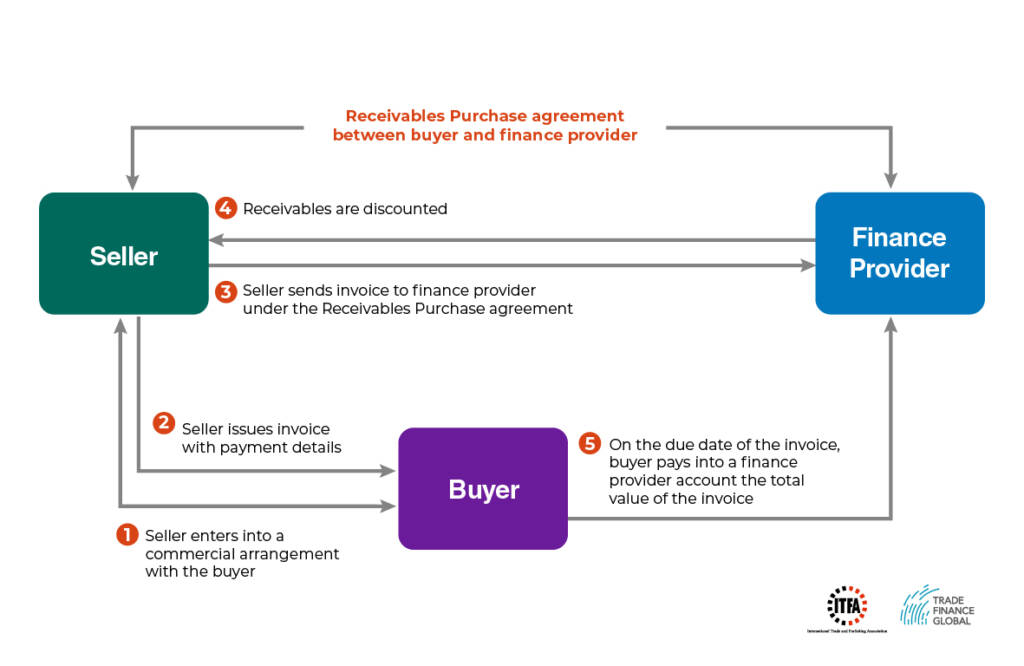

Diagram: How invoice finance (receivables purchase) works

How can invoice finance benefit my business?

- The invoice financier will sometimes take on the responsibility to look after your sales ledger which means the business owner can have more time to focus on the business

- An invoice financier will conduct due diligence (including credit checks) on customers, which reduces the risk of not receiving funding

- Invoice discounting can be done on a confidential arrangement, which means that your customers will not know that you’re using a finance house; this can help protect your reputation

- Invoice finance allows you to maintain a good relationship with your customers, as you can fulfill larger orders on time without worrying about cash flow and working capital problems

How can we help?

The TFG’s invoice finance team work with the key decision-makers at 270+ banks, funds and alternative lenders globally, assisting companies in accessing factoring and discounting facilities.

Our team are here to help you scale up to take advantage of both domestic and international opportunities. We have product specialists, from commodities to finished goods.

Often the financing solution that is required can be complicated, and our job is to help you find the appropriate invoice finance solutions for your business.

Read more about Trade Finance Global and our team.

Our Invoice Finance Client Case Studies

Get started – talk to our team

Contact Information

If you have an invoice finance enquiry, please use the contact form.

Otherwise, you can reach us on the email addresses below.

Trade Finance Global

201 Haverstock Hill

Second Floor

London

NW3 4QG

Telephone: +44 (0) 2071181027

Invoice & Receivables Finance Enquiries

Want to learn more about invoice finance?

You’ve come to the right place. Here you can find our latest features, research and trending articles in the world of invoice finance. Sit back, and catch up with the latest thought leadership and interviews from the TFG, listen to podcasts and digest the top stories in invoice finance right below.

From the Editor - Invoice Finance Insights

Factoring and supply chain finance in the shadow of the Areni-1 cave: EBRD’s insights from Yerevan – The EBRD TFP conference gathered industry leaders to discuss evolution of factoring and supply chain finance in emerging markets.

Factoring and supply chain finance in the shadow of the Areni-1 cave: EBRD’s insights from Yerevan – The EBRD TFP conference gathered industry leaders to discuss evolution of factoring and supply chain finance in emerging markets. PODCAST | FCI’s Neal Harm on kicking off inclusive growth in the factoring industry – To better understand the principles of financial inclusion, equitable regulation, and sustainable growth in the factoring industry, Trade Finance Global’s (TFG) Deepesh Patel spoke with new FCI Secretary General, Neal Harm.

PODCAST | FCI’s Neal Harm on kicking off inclusive growth in the factoring industry – To better understand the principles of financial inclusion, equitable regulation, and sustainable growth in the factoring industry, Trade Finance Global’s (TFG) Deepesh Patel spoke with new FCI Secretary General, Neal Harm.  Bridging the gap: The transformative potential of factoring in Africa – Factoring in Africa allows businesses to sell their accounts receivable at a discount to gain immediate cash flow, is gaining traction across the continent, buoyed by significant growth and the support of institutions like Afreximbank and FCI.

Bridging the gap: The transformative potential of factoring in Africa – Factoring in Africa allows businesses to sell their accounts receivable at a discount to gain immediate cash flow, is gaining traction across the continent, buoyed by significant growth and the support of institutions like Afreximbank and FCI.Latest Insights

Videos - Invoice Finance

Invoice Finance Podcasts

Hub Articles

- Invoice Finance for SMEs

- Comparing Invoice Finance Providers

- Invoice Factoring versus Invoice Discounting

- Recourse or Non-Recourse Factoring?

- Bill Discounting and Factoring

How to use Invoice Financing for your Small Business

Invoice factoring for small businesses is fairly straightforward. As an example, an end customer might not pay the £100,000 invoice issued to them for up to 90 days, but your company needs the funds in 2 weeks, in order to pay for business expenses and salaries.

How to use Invoice Financing for your Small Business

Why should I compare invoice factoring or invoice discounting providers?

There are several bank and non-bank providers of invoice finance, from large instutions to small alternative funders, each offering different propositions and solutions for customers.

What is the difference between invoice factoring and invoice discounting?

Invoice factoring and invoice discounting are both types of asset backed finance aimed to help businesses release cash which are tied in invoices.

What is the difference between recourse factoring and non recourse factoring?

The industry defines the two forms of factoring by risk. Invoice finance is effectively a line of credit obtained on the value of your outstanding sales ledger. Here’s what happens if your debtors fail to pay the invoices after you have financed them.

What is bill discounting and how does it differ from factoring?

Bill discounting, also known as purchase of bills and invoice discounting are all the same type of financial instrument used to provide working capital to small and medium enterprises from invoices raised.

Invoice Finance - Frequently Asked Questions

Invoice finance is a type of receivables finance, which includes factoring and discounting.

Factoring is present when a business assigns their invoices to a third party and the factoring company has full visibility of the sales ledger and will collect the debts when due.

- The customer has knowledge that the invoices have been factored. (This is the typical route a lot of funders offer, however – some can offer Confidential Factoring)

- Factoring gives businesses up to 90% pre-payment against submitted invoices

- This enables improved cashflow, and reduces the need to wait for payment

- The company may receive their funds up to two days after invoices are sent out. Many factoring companies will offer to send money same day (TT Payment, usually carries a charge) or by BACS (Free)

- A business can choose a ‘selective’ factoring or invoice discounting facility, dependent on the funder.

Typically, with Invoice Discounting, the borrower will have more control over their ledger. Again – like factoring, there is the option to do this on a completely confidential basis.

- Invoice discounting is an alternative way of drawing money against the invoices of a business

- The business retains control over the administration of their sales ledger

- Invoice discounting usually involves a company reconciling with their invoice financier monthly

- With factoring – each individual invoice is uploaded – with Invoice Discounting, a bulk figure is uploaded and then drawn down against with the monthly reconciliations showing where money is allotted to

- Under a selective facility a business can opt to factor (i.e. lend) or invoice discount just some of the submitted invoices

- A selective facility is a good option if a business needs a certain amount of cashflow guaranteed each month or if one or two customers are good payers.

The main difference between factoring and invoice discounting is that with factoring, a funder will have full visibility of your sales ledger and maintain this by chasing debts on your behalf. Invoice discounting on the other hand, allows you to keep your credit control in house but as we already discussed, it would require a monthly reconciliation with the invoice financier. Naturally, management fees for invoice discounting are usually a lot lower, however a company must demonstrate they have the correct procedures in place to support an Invoice Discounting facility.

Factoring solutions offer the seller of a receivable a wider service than just the advance of funds to shorten its cash conversion cycle as the entity buying the receivable will also usually take on the responsibility of collecting the debt.

Factoring can take several forms. For example, a factor may agree, subject to limits, to buy the whole of a seller’s receivables. This is known as whole turn-over factoring. Conversely, a factor may select which invoices he wishes to buy. It can be with or without recourse to the seller and may or may not be notified to the buyer or obligor.

The vast majority of factoring is domestic and individual invoices are often of a low value. Cross-border factoring is possible using the two-factor system. One factor is in the buyer’s country (known as the ‘Import Factor’) and the other in the seller’s country (known as the ‘Export Factor’). The two Factors establish a contractual or correspondent relationship to service the buyer and the seller respectively under which the Import Factor in effect, guarantees the receipt of funds from the importer and remits payment to the Export Factor. Typically, the two factors use an established framework such as the General Rules for International Factoring (GRIF), provided by FCI. Read more about factoring here.

Invoice discounting solutions tend to focus on shortening a seller’s cash conversion cycle, as opposed to encompassing debt management and collection aspects. The degree of disclosure to the debtor under this type of facility varies, ranging from full disclosure to no-disclosure, depending on the level of comfort taken by the purchaser of the receivables over the nature and standing of the seller. In most cases, the greater the control the financing entity/purchaser of the receivables manages to attain over the process, the better the discounting conditions offered.

An invoice discounting facility without disclosure to the debtor will grant the seller of the receivables full confidentiality, and therefore avoid reputational hazards. Most invoice discounting is without recourse to the seller so as to ensure de-recognition of the receivables from the seller’s balance sheet (so-called “true sale”) but recourse is normally retained for commercial dispute e.g. where the buyer refuses to pay because the goods or service are defective. Read more about invoice discounting here.

Rather than waiting 30 – 90 days, an invoice financier can pay for most of the invoice amount up front, and the interest rate is the amount charged for this service. Interest rates are often linked to base rates the bank will pay for borrowing money, such as the LIBOR, as well as a management fee.

At first instance, invoice finance lenders can advance around 90% of the invoice amount value up front, whether that be through invoice discounting or factoring. Once the invoices are paid by the end customer, the borrower will be paid the remaining difference, excluding interest rate and management fees. Even if the company has existing finance arrangements such as an existing bank loan or overdraft, invoice discounting or factoring may still work for a business.

Normally, a lender will analyse the business prior to implementing a factoring or invoice finance facility. They may audit the financial records of the business and list the approved customers, and the decision is down to legal and contractual implications such as security and existing lenders.

The company should always read the offer letter and look at all (including the following) costs:

- Discount costs

- Service or management fees (including the minimum service fee which is normally derived as a % of the service fee)

- Audit charges

- Re-factoring charges

- Transactional costs

- Notice period for ending service and associated fees

- Annual service costs

- Trust account costs

- Additional costs for services such as credit protection

There are three parties involved directly in invoice finance:

- the funder who advances money against the invoice or receivable

- the business (or customer) who sends out the invoice

- and the debtor who is required to pay for the invoice

A brief explanation: The receivable, associated with the invoice for services or goods acts as an asset and provides the company the legal right to collect money from the debtor. A percentage of funds are then advanced against the value of the invoice.

Strategic Partners:

Get in touch with our Invoice Finance team

Invoice Finance Hub – Contents

1 | Invoice Discounting

2 | Factoring

3 | Receivables Factoring

4 | Receivables Finance

5 | Receivables Discounting

6 | Accounts Receivables Finance

7 | Accounts Receivables

Download our free invoice finance guide

Our factoring and invoice finance partner

Latest News

Factoring and supply chain finance in the shadow of the Areni-1 cave: EBRD’s insights from Yerevan

0 Comments

PODCAST | FCI’s Neal Harm on kicking off inclusive growth in the factoring industry

0 Comments

Bridging the gap: The transformative potential of factoring in Africa

0 Comments

PODCAST | Year ahead: Swift CIO on balancing uneven payments regulation and advancing CBDC

0 Comments

Switching the Pound for the Peso: Three reasons why you should consider settling invoices in local currencies

0 Comments

FCI scores hat-trick in Marrakesh: A giant leap for factoring

0 Comments

A common credit insurance hub: The solution to streamline credit insurance?

0 Comments

ISO 20022: A game changer for Canadian corporations

0 Comments

Global invoice factoring market poised for exponential growth by 2032

0 Comments

PODCAST | Breaking: First cross-border factoring facility between Armenia and Georgia supported by EBRD

0 Comments

PODCAST | Factoring in the UAE: Developments and global implications

0 Comments

Evolution of electronic invoicing: watch for the explosive growth

0 Comments

VIDEO | Visa: the highs and lows of B2B payments

0 Comments

Bill discounting vs. invoice factoring – what’s the difference?

0 Comments

Driving sustainability in global trade with digital collaboration

0 Comments

While the… Read More →

World of Open Account (WOA) cofounders on the changing face of receivables finance

0 Comments

What is structured trade finance (STF)?

0 Comments

Is the time ripe for the formation of a global receivable exchange?

0 Comments

SME appetite for trade finance

0 Comments

Podcast: FCI – why the factoring industry is experiencing a boom

0 Comments

Debt vs. equity finance: how do European SMEs use third-party financing?

0 Comments

City Week exclusive: Bob Wigley on UK SME lending in 2022

0 Comments

VIDEO: Factoring strikes back – FCI’s Aysen Çetintas on expanding trade finance education after COVID-19

0 Comments

Explained: How these 5 trade finance instruments can help your business grow in 2022

0 Comments

2021 – A Year in Review with Trade Finance Global

0 Comments

Do you export? Take part in our access to finance survey

0 Comments

South Africa’s Standard Bank chooses Flutterwave for Africa digitalisation drive

0 Comments

BNP Paribas executes green repurchase agreement (repo) with EDF

0 Comments

Can SMEs benefit from digital solutions in trade finance?

0 Comments

FCI Launches 53rd Annual Meeting through new virtual platform

0 Comments

Visit our Global Hubs

Australia 🇦🇺

France 🇫🇷

Germany 🇩🇪

Hong Kong 🇭🇰

India 🇮🇳

Ireland 🇮🇪

Japan 🇯🇵

Netherlands 🇳🇱

Singapore 🇸🇬

United Arab Emirates 🇦🇪

United States of America 🇺🇸