Australia

Australia Hong Kong

Hong Kong Japan

Japan Singapore

Singapore United Arab Emirates

United Arab Emirates United States

United States France

France Germany

Germany Ireland

Ireland Netherlands

Netherlands United Kingdom

United Kingdom

What are the types of trade finance lenders?

Trade finance providers can broadly be split into banks and non-bank lenders (funds and alternative financial institutions).

When accessing trade finance, it is crucial that business owners choose a suitable lender among the different types of trade service providers on the market.

1. Banks

Banks account for the majority of financial institutions globally, although they range in size from small regional operators to large multinationals.

Banks are a popular source of trade finance because their cost of borrowing is often lower than most alternative lenders.

However, a bank is usually under heightened regulatory pressure, so there are longer decision timeframes and less flexibility.

The specific trade finance services that banks offer will vary, but will usually include services such as issuing bills of exchange or letters of credit and accepting drafts and negotiating notes.

Two main types of banks provide trade finance: large corporate and investment banks (CIBs) and smaller commercial banks.

The main difference between CIBs and smaller commercial banking is the size of the clients, with CIBs generally serving larger clients and larger transactions, while commercial banks tend to cater to a wider range of smaller clients.

Corporate and investment banks (CIBs)

These banks typically manage larger clients and transactions, and their strong global reputation means that they can provide cross-border services at a lower cost than smaller banks.

Some larger commercial banks also have specialised trade finance divisions that offer trade services and debt facilities.

Commercial banks

Smaller domestic banks can be advantageous to SMEs because their financial products may be more flexible and tailored to specific niche categories and verticals.

As with any bank, however, heightened regulatory pressures can make their decision-making process more time-consuming and less flexible.

Alternative finance providers and non-bank lenders

These lenders tend to be unregulated, which means their processes are often faster than traditional banks.

However, because many of them raise funding from sources such as banks, private investment, and crowd-funded (pooled) investment, the cost of the finance they offer can be significantly higher.

New technologies and platforms have been developed to disrupt the traditional lengthy application processes for trade finance products – including risk assessment, documentation to importers and exporters and supply credit.

Examples of alternative providers include development finance institutions (DFIs) and export credit agencies (ECAs).

Development finance institutions (DFIs)

Also known as development banks or development finance companies (DFCs), these institutions typically provide finance as a way to generate or promote economic development.

Often this is for mid-to-long-term projects, such as in the agricultural or mining sectors.

DFIs usually operate as joint ventures in emerging markets, where they encourage investment and provide insurance and guarantees against political and socio-economic risks.

They can also supply standby letters of credit (SBLCs), invoice discounting facilities, and project finance.

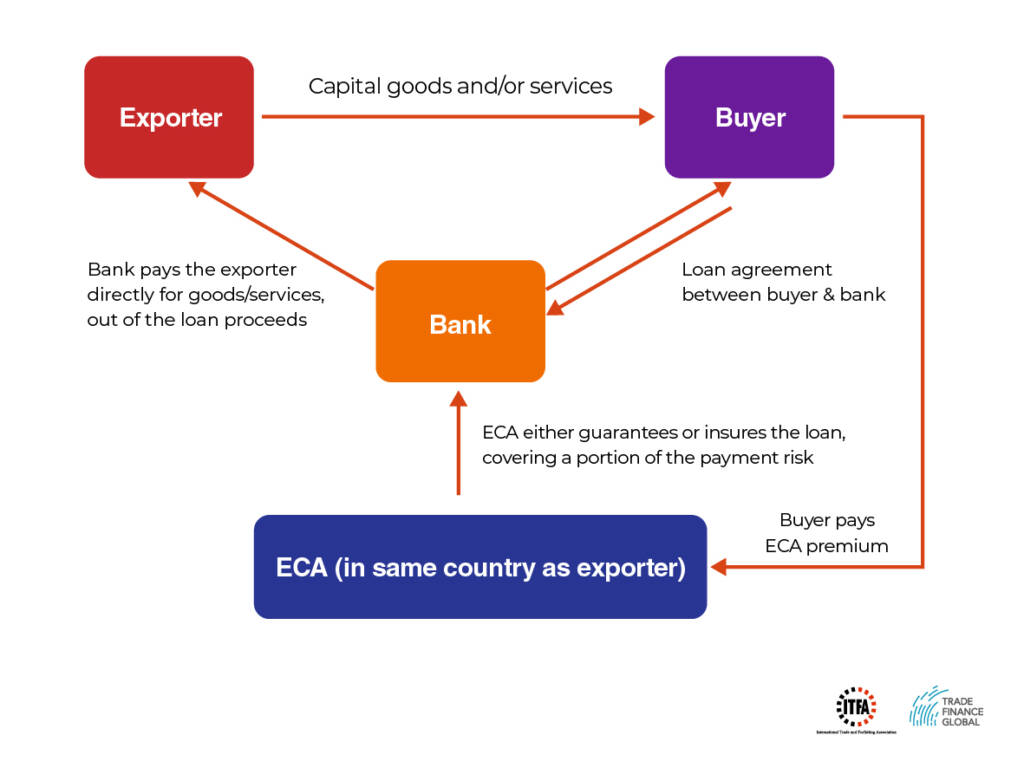

Export credit agencies (ECAs)

These are government-backed institutions – like UK Export Finance (UKEF) in the UK or Export Development Canada (EDC) in Canada – that guarantee a domestic company’s exports.

They tend to structure their finance and insurance around non-conventional risks, such as overseas commercial liabilities and political risk.

Find out more about the different ECAs around the world on our ECA hub.

Latest ECA insights

ECAs play a vital role in protecting international trade flows – ECAs play a critical role in promoting and shoring up international trade flows, particularly during times of upheaval and economic stress.

ECAs play a vital role in protecting international trade flows – ECAs play a critical role in promoting and shoring up international trade flows, particularly during times of upheaval and economic stress. Addressing Africa’s debt dilemma: The role of ECAs and new strategies – Learn about the debt crisis that African governments are facing & the need to renegotiate debts in order to avoid defaulting.

Addressing Africa’s debt dilemma: The role of ECAs and new strategies – Learn about the debt crisis that African governments are facing & the need to renegotiate debts in order to avoid defaulting. PODCAST | Empowering the American dream: SBA’s trade finance solutions for U.S. exporters – Discover how the SBA is committed to helping small businesses enter the international trade market on this episode of Trade Finance Talks.

PODCAST | Empowering the American dream: SBA’s trade finance solutions for U.S. exporters – Discover how the SBA is committed to helping small businesses enter the international trade market on this episode of Trade Finance Talks. Is trade and receivables finance the new home for private credit? – The financial landscape has undergone a seismic shift in recent years. From zero or negative interest rates to the COVID-19 pandemic and geopolitical tensions, the world has seen it all. Amidst this backdrop, the role of private credit has evolved significantly.

Is trade and receivables finance the new home for private credit? – The financial landscape has undergone a seismic shift in recent years. From zero or negative interest rates to the COVID-19 pandemic and geopolitical tensions, the world has seen it all. Amidst this backdrop, the role of private credit has evolved significantly.  The critical need for short-term credit insurance in West Africa – Micro, small and medium-sized businesses are the backbone of employment and economic growth in West Africa. How can short-term credit insurance help these businesses to grow and prosper?

The critical need for short-term credit insurance in West Africa – Micro, small and medium-sized businesses are the backbone of employment and economic growth in West Africa. How can short-term credit insurance help these businesses to grow and prosper? Credit insurance, export credit and funds: How do we solve the African trade finance gap? (Part 1) – Africa, a continent synonymous with immense economic growth potential and abundant opportunities, has long grappled with transforming that potential into tangible growth. Despite being hailed as a land of promise, the realisation of Africa’s vast potential has remained elusive year after year.

Credit insurance, export credit and funds: How do we solve the African trade finance gap? (Part 1) – Africa, a continent synonymous with immense economic growth potential and abundant opportunities, has long grappled with transforming that potential into tangible growth. Despite being hailed as a land of promise, the realisation of Africa’s vast potential has remained elusive year after year.

Trade Finance Hub

1 | Introduction and the benefits

2 | Types of trade financing

3 | Methods of payment

4 | Pre and post-shipment finance

5 | Risks and challenges

6 | Trade and export finance providers

7 | The credit process and securing finance

8 | SME Trade Finance Guide